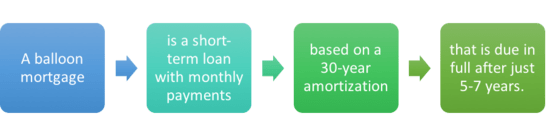

A balloon mortgage is a type of loan that has a shorter duration than traditional mortgages, and requires borrowers to pay a large lump sum at the end of the loan. This type of financing is appealing for those who need a lower monthly payment, but may need to be prepared to pay off the loan balance in full when the time comes. By understanding the basics of balloon mortgages, you can make an informed decision to determine if this type of loan is right for you.

Introduction to Balloon Mortgages

A balloon mortgage can be a great option if you’re looking to save money on your monthly payments. This type of mortgage allows you to pay off a large portion of your loan in one large payment at the end of the term. The lower monthly payments make it easier to manage your finances while still allowing you to put money towards other investments. With a balloon mortgage, you get the benefit of a lower interest rate and monthly payment, but you must be prepared to pay off the remaining balance at the end of the term. If you’re looking for a way to save money on your mortgage, a balloon mortgage might be the perfect solution.

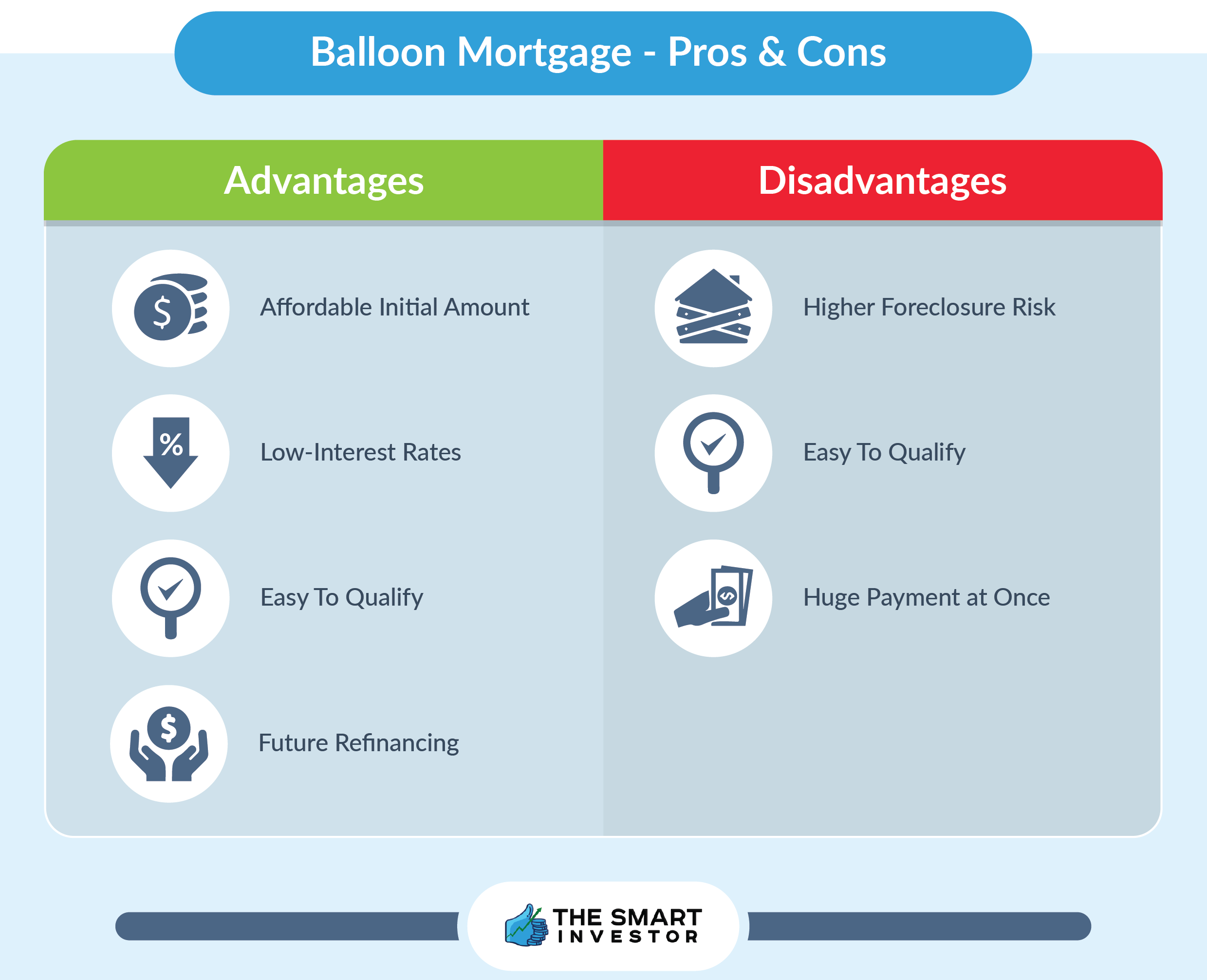

Advantages and Disadvantages of Balloon Mortgages

Advantages of Balloon MortgagesBalloon mortgages have some great advantages that make them attractive to many borrowers. First, the interest rates on balloon mortgages are usually lower than those on traditional mortgages, resulting in lower monthly payments. Another advantage is that balloon mortgages often have shorter terms, meaning you can get out of your mortgage and into a new one much sooner. Finally, balloon mortgages are great for those who don’t plan to stay in their homes for a long period of time. Since balloon mortgages require the entire balance to be paid off at the end of the term, you can easily move on to a new home without worrying about the remaining balance on your mortgage.Disadvantages of Balloon MortgagesDespite their advantages, balloon mortgages also have some drawbacks. First and foremost, you will have to pay the entire balance of the loan at the end of the term. This can be a huge financial burden if you’re not able to secure a new loan or refinance your existing one. Additionally, the lower monthly payments of balloon mortgages can lead to an increase in total interest paid over the life of the loan. Finally, if you’re uncertain of your future financial situation, a balloon mortgage may not be the best option as you may

Qualifying for a Balloon Mortgage

Qualifying for a balloon mortgage can be a tricky process. You’ll need to have a steady income and a good credit score in order to be approved. You also need to be prepared for the fact that you’ll be paying a larger amount of money at the end of your loan term. It’s important to make sure that you’ll be able to handle the payment when it comes due, so make sure you do your research and get an idea of how much you’ll need to pay. It’s also important to make sure that your monthly payments are manageable and that you’re not overextending yourself financially. If you’re able to meet all the requirements, then you could find that a balloon mortgage could be a great way to finance a home purchase.

When to Consider a Balloon Mortgage

When it comes to deciding if a balloon mortgage is right for you, there are a few things to consider. Are you looking for a short-term loan with a lower interest rate, or are you looking for a loan with a longer-term that you can pay back over a longer period of time? Also, do you have a plan for how you will pay off the balloon payment at the end of the loan? If you do not have a plan for how you will pay off the balloon payment, then a balloon mortgage may not be the best choice for you. If you are looking for a way to get a lower interest rate for a short-term loan, then a balloon mortgage may be worth considering. Just make sure you have a plan in place to pay off the balloon payment when it comes due.

Common Questions about Balloon Mortgages

If you’re thinking about getting a balloon mortgage, you probably have a lot of questions. A balloon mortgage is a unique type of home loan with a pretty large payoff at the end of the loan term. You may be wondering how much of a down payment you need, if your interest rate will be fixed or adjustable, and what kind of fees you can expect. All of these questions are important to consider before you take out a balloon mortgage, so let’s explore some common questions about this type of loan. First, it’s important to ask how much of a down payment is necessary for a balloon mortgage. Generally, you’ll need to put down at least 10% of the home’s purchase price as a down payment. This can vary based on the lender, so be sure to do your research and shop around. When it comes to interest rates, balloon mortgages typically come with either a fixed or adjustable rate. A fixed rate means your interest rate will remain the same throughout the life of the loan, while an adjustable rate may change over time. Be sure to ask your lender what type of rate you’ll be getting so you know what to expect. Finally,