Mortgage insurance is an essential component of many home buyers’ financial journeys, but do you know what it is and why it’s so important? This article will explain what mortgage insurance is, what it does, and the advantages and disadvantages of having it. It will also provide information about the different types of mortgage insurance and how to decide if it’s the best option for you. Whether you’re a first-time home buyer or you’re looking to refinance, understanding mortgage insurance can help you make the best decisions for your personal financial goals.

What is Mortgage Insurance and How Does it Work?

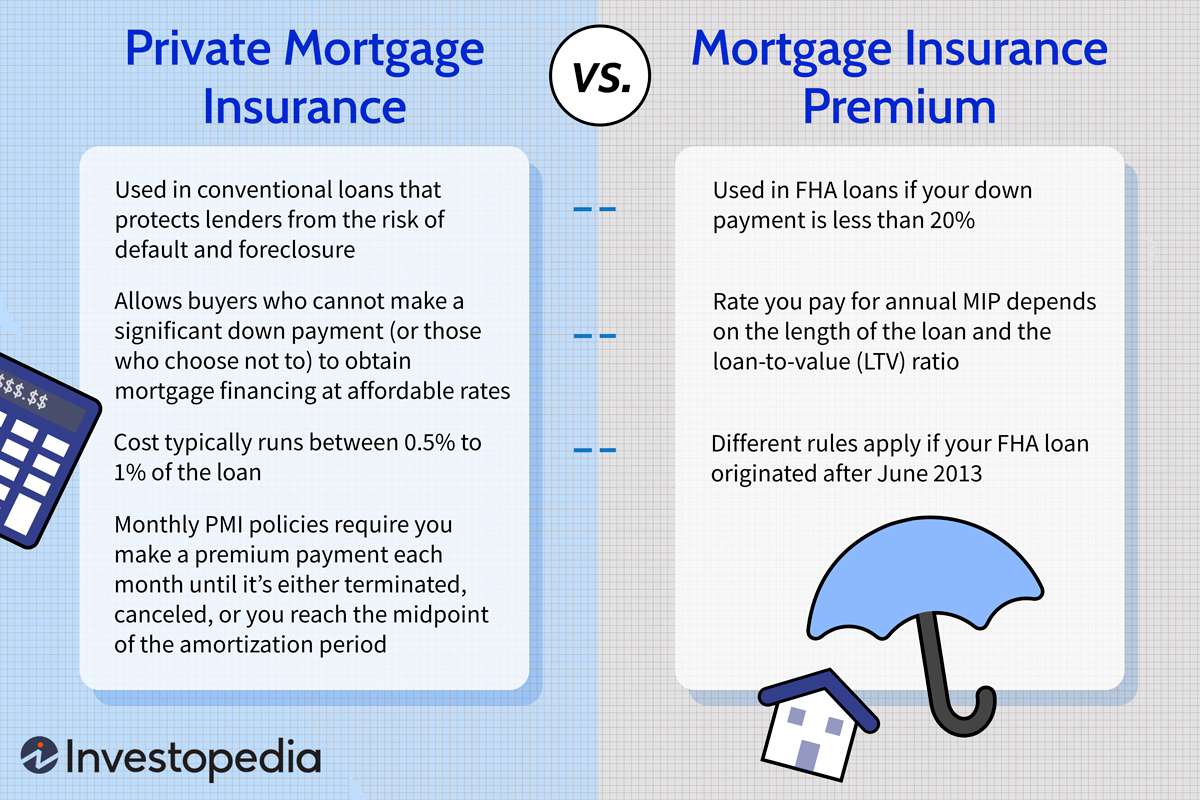

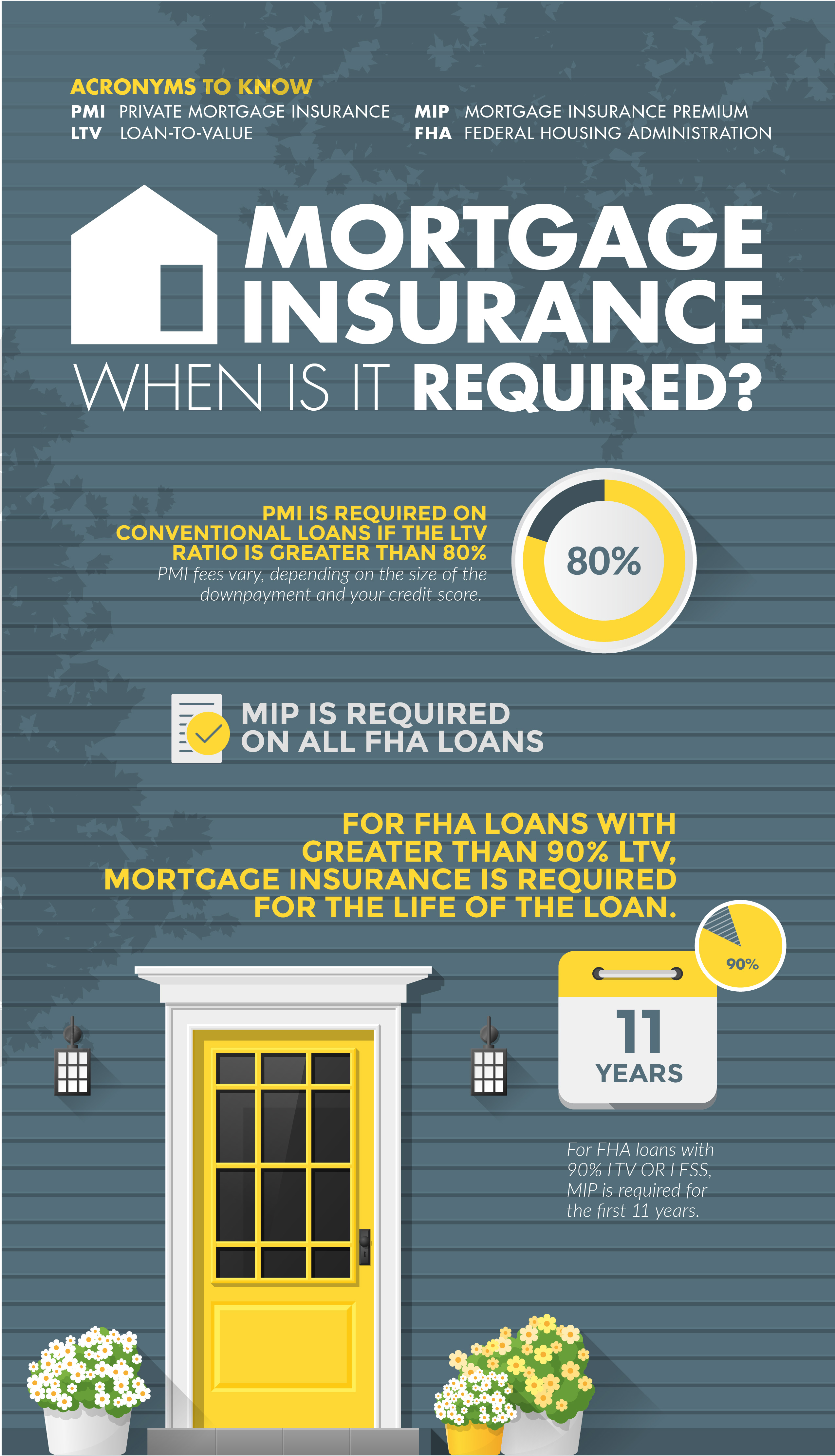

Mortgage insurance is an insurance policy that protects lenders from the risk of default on a mortgage loan. The insurance, which is typically paid for by the borrower, typically covers the lender for any losses that may occur if the borrower is unable to repay the loan. It is usually required by lenders when the borrower has a down payment of less than 20 percent of the purchase price of the home.Mortgage insurance works by protecting the lender in the event of a default on the mortgage loan. When the borrower pays their mortgage insurance premiums, the lender is provided with a guarantee in the event of a default. This guarantee covers the lender for any losses that may occur due to the borrower’s inability to repay the loan. The insurance is typically paid for by the borrower, which can be a one-time payment or a series of monthly payments.Mortgage insurance can be beneficial for both the borrower and the lender. For the borrower, it allows them to take out a loan with a lower down payment than would otherwise be required. This could potentially save them money in the long run. For the lender, the insurance provides them with a degree of security and assurance that the loan will be repaid, even if the borrower defaults.

Who Needs Mortgage Insurance?

Mortgage insurance is a type of insurance that protects lenders in the event of a borrower defaulting on their mortgage loan. It is usually required when a borrower has a down payment of less than 20% of the total home purchase price. Who needs mortgage insurance? Generally, any borrower that does not have the required down payment amount of 20% should be prepared to pay for mortgage insurance. This includes first-time home buyers, those refinancing their mortgage or those taking out a second mortgage.In addition, those with a higher loan-to-value ratio, such as those taking out a large loan amount relative to the home value, will often be required to purchase mortgage insurance. Those with a poor credit score or non-traditional income may also need to purchase mortgage insurance. Borrowers in these situations are considered higher-risk by lenders, and so they will often require mortgage insurance to protect them in case of a borrower’s default. Since mortgage insurance is usually required when a borrower has a down payment of less than 20%, it is important for borrowers to understand the costs associated with mortgage insurance. It is typically an additional expense, and will be added to your monthly mortgage payments. The amount of mortgage insurance can vary depending on

Types of Mortgage Insurance

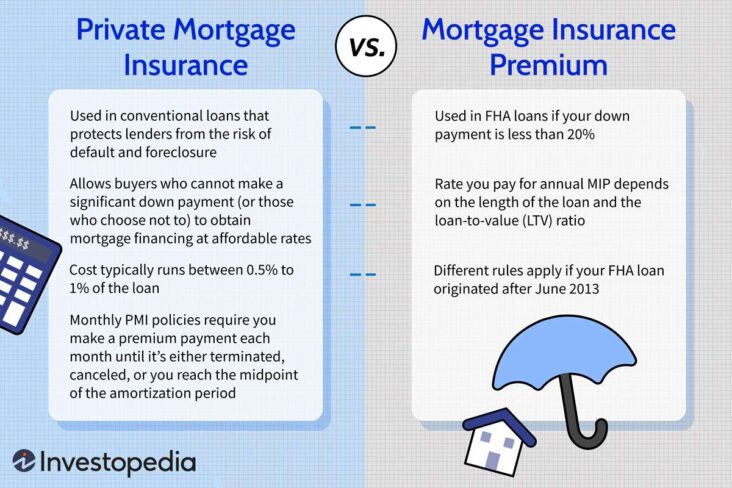

Mortgage insurance is an important type of coverage that helps protect mortgage lenders and borrowers in the event of a loan default. There are two main types of mortgage insurance: private mortgage insurance (PMI) and mortgage insurance premiums (MIP).PMI is a type of insurance that borrowers may be required to purchase if they’re unable to make a 20% down payment on a home. PMI protects lenders in the event of a borrower defaulting on their mortgage loan. The cost of PMI varies depending on the size of the loan and the borrower’s credit score.MIP is a type of mortgage insurance required for borrowers who take out a home loan with an FHA (Federal Housing Administration) loan. MIP is paid upfront and annually as part of the loan, and it protects the lender in the event of a loan default. The cost of MIP depends on the size of the loan and the length of the loan term.Mortgage insurance helps to protect lenders and borrowers in the event of a loan default. It is important to understand the different types of mortgage insurance and the costs associated with each type, to ensure that you are making the right decision when it comes to financing your home.

The Pros and Cons of Mortgage Insurance

Mortgage insurance is a beneficial tool for many homebuyers but it’s important to understand the pros and cons before committing to it. One of the major pros of mortgage insurance is that it can make it easier to qualify for a loan and can even enable borrowers to purchase a home with a lower down payment. Mortgage insurance also provides protection for lenders, so they are more willing to offer loans to borrowers with less than perfect credit. The most common type of mortgage insurance is private mortgage insurance (PMI), which is a policy purchased by the borrower and paid for with a monthly premium. On the other hand, one of the cons of mortgage insurance is that it can be costly and will increase the amount of the loan payments. Additionally, if you are able to pay off the loan before the mortgage insurance is no longer required, you will not receive any of the money you paid for the insurance. It’s important to weigh the pros and cons of mortgage insurance before making a decision and to talk to a financial advisor for advice.

How to Save Money on Mortgage Insurance

Saving money on mortgage insurance is possible and can be done in a few different ways. First, it is important to understand that mortgage insurance is typically required when you have a down payment of less than 20%. By increasing your down payment, you can reduce the amount of mortgage insurance you need to pay. In addition, it is also important to shop around for the best rates and terms when it comes to mortgage insurance. Another way to save money on mortgage insurance is to look into government programs such as the Federal Housing Administration (FHA). FHA loans generally come with lower mortgage insurance premiums than conventional loans. Finally, if you have a good credit score, you may be able to get a better rate on your mortgage insurance. A higher credit score means a lower risk for the lender, and thus a lower rate for you. By taking the time to explore these options, you can save yourself a significant amount of money on mortgage insurance.