Are you considering taking the plunge into homeownership but feeling overwhelmed by the myriad of mortgage options available? Fear not, as we’re here to guide you through one popular financing choice: the FHA loan. Designed to help first-time homebuyers and those with less-than-perfect credit, FHA loans come with their own unique set of advantages and drawbacks. In this comprehensive article, we’ll explore the pros and cons of FHA loans, enabling you to make an informed decision about whether this government-backed mortgage program is the right fit for your homeownership journey. So, buckle up and prepare to become an FHA loan expert in no time!

Low down payment requirements: One of the primary benefits of an FHA loan is the low down payment requirement

Low down payment requirements are a significant advantage of FHA loans, making homeownership more accessible for many aspiring buyers. This feature is particularly appealing to first-time homebuyers or those with limited savings, as the minimum down payment for an FHA loan is only 3.5% of the purchase price. Compared to conventional loans, which typically require a 5-20% down payment, FHA loans offer a more affordable entry point into the real estate market. This lower initial investment not only helps borrowers preserve their savings but also enables them to start building equity in their homes sooner. As a result, the reduced down payment requirement of FHA loans is a key factor that continues to attract prospective homebuyers.

Borrowers can put as little as 3.5% down on their home, making it easier for first-time homebuyers or those with limited savings to enter the housing market.

One of the key advantages of an FHA loan is the low down payment requirement, which allows borrowers to put down as little as 3.5% on their home purchase. This significantly eases the financial burden for first-time homebuyers or individuals with limited savings, enabling them to enter the housing market sooner. By reducing the upfront costs associated with homeownership, FHA loans provide an accessible pathway to achieving the dream of owning a home for many aspiring buyers. Additionally, this lower down payment requirement can help borrowers maintain a healthy financial cushion for future expenses, such as home maintenance or unexpected emergencies.

Flexible credit requirements: FHA loans have more lenient credit requirements than conventional loans, which means those with lower credit scores can still qualify for financing

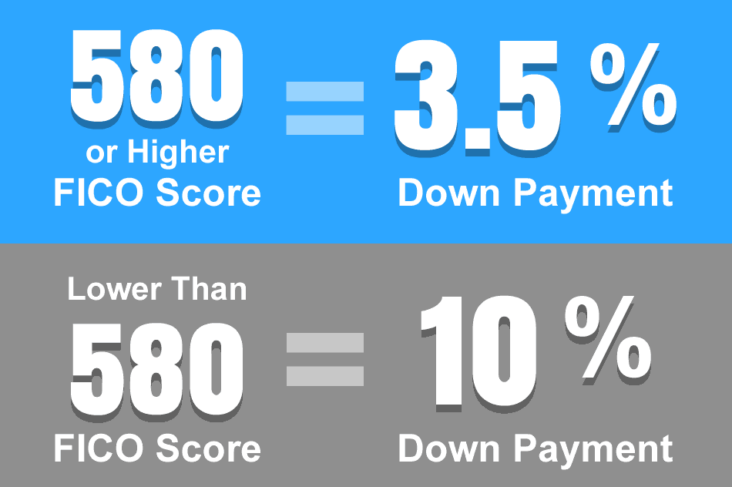

Flexible credit requirements are a significant advantage of FHA loans, as they cater to borrowers with less-than-perfect credit. Unlike conventional loans, which typically demand higher credit scores, FHA loans allow individuals with lower credit ratings to secure financing for their dream home. This inclusive approach enables a broader range of potential homeowners to enter the property market, promoting economic growth and stability. With the possibility of qualifying for an FHA loan with a credit score as low as 500, this option becomes accessible to a wider audience, making homeownership a reality for many who may have otherwise been denied a conventional mortgage.

Borrowers with a credit score as low as 580 can potentially secure an FHA loan with a 3.5% down payment.

Borrowers with credit scores as low as 580 can potentially secure an FHA loan with a minimal 3.5% down payment, making homeownership more accessible for those with less-than-perfect credit. This low credit score requirement provides an opportunity for individuals to rebuild their credit while simultaneously investing in a property. By offering a lower down payment, FHA loans also reduce the initial financial burden for prospective homebuyers. However, it is essential to note that borrowers with lower credit scores may face higher interest rates, which could increase the overall cost of the loan. Therefore, prospective borrowers should carefully weigh the benefits and potential drawbacks of an FHA loan based on their unique financial situation and credit history.

Assumable loans: FHA loans are assumable, meaning that if a homeowner decides to sell their house, the buyer can take over the

One notable advantage of FHA loans is that they are assumable, allowing potential homebuyers to take over the existing mortgage when purchasing a property. This feature can be particularly beneficial during times of rising interest rates, as the buyer can benefit from the lower interest rate locked in by the original borrower. In addition, assuming an FHA loan can result in lower closing costs and reduced qualification requirements for the buyer. However, it’s essential to keep in mind that not all FHA loans are assumable, and the lender must approve the transaction for this option to be viable. In summary, assumable FHA loans can provide significant benefits for both buyers and sellers, but it’s critical to thoroughly research and understand the specific terms and conditions.