Are you considering taking out a mortgage loan? If so, you may have heard of mortgage insurance premium (MIP). In this article, we’ll break down exactly what MIP is, why it’s important, and how it affects your mortgage loan. By the end, you’ll have a better understanding of MIP and how it can affect your loan. So, let’s dive in!

Understanding Mortgage Insurance Premium

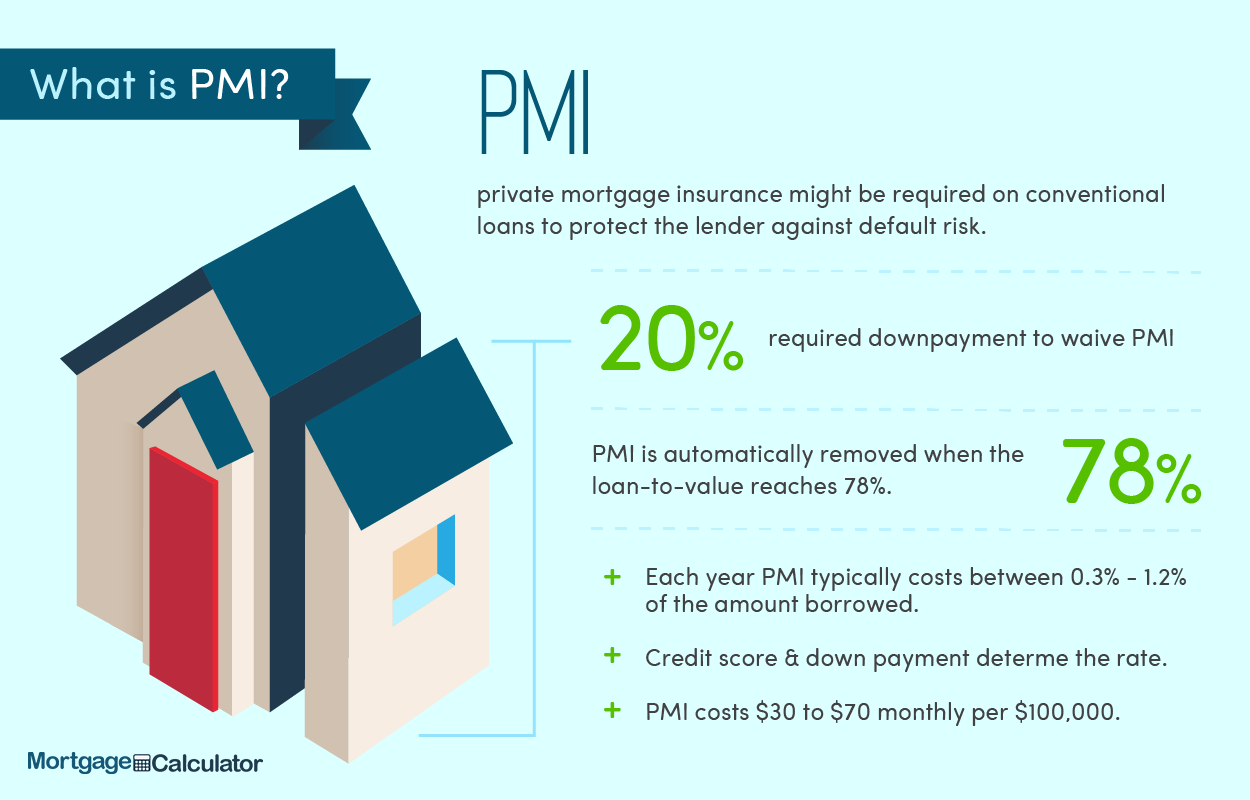

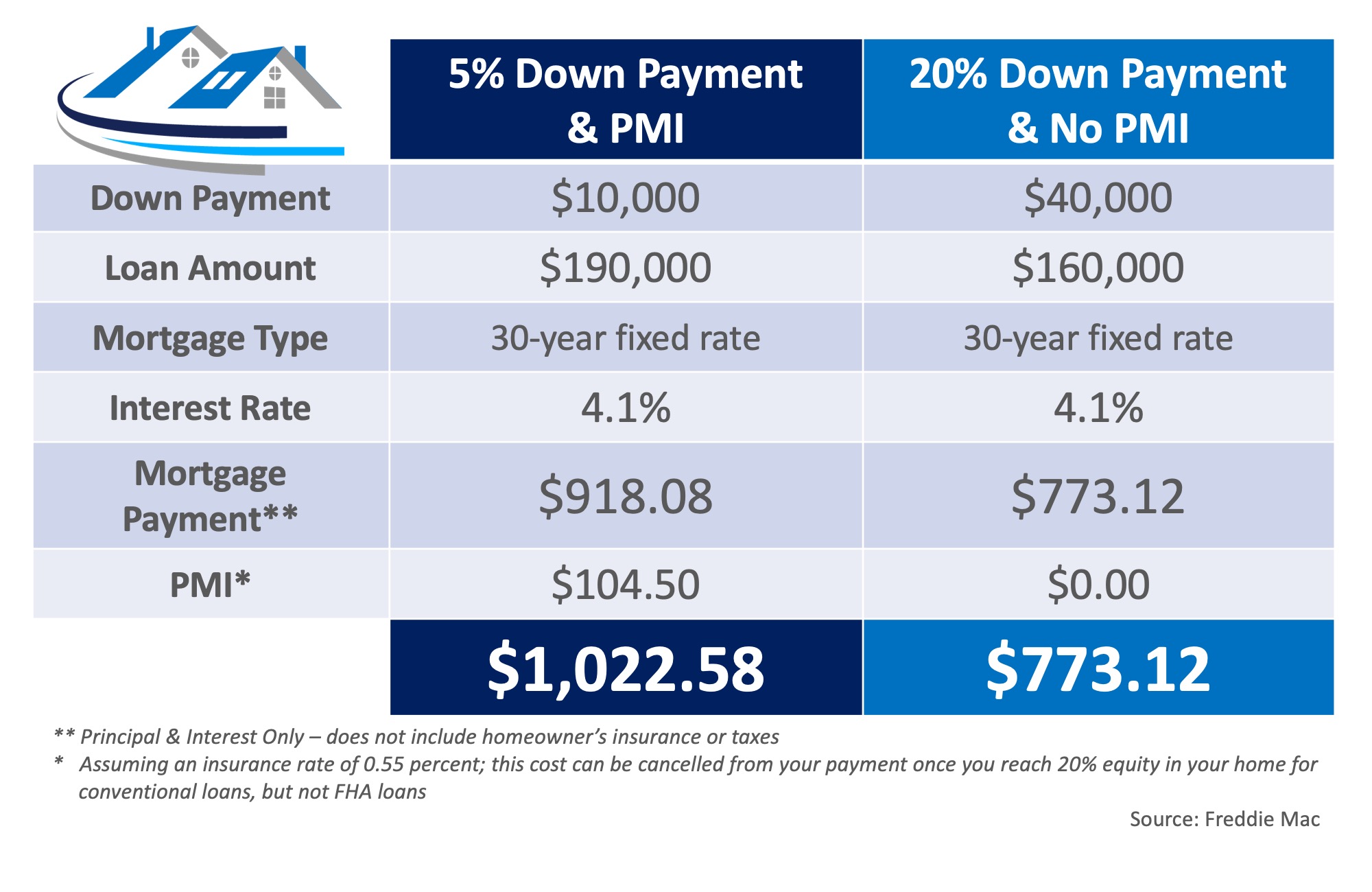

Mortgage insurance premium (MIP) is a type of insurance that helps protect lenders from potential losses due to default on a mortgage loan. MIP is typically required for loans with a loan-to-value ratio of greater than 80%. This means that if the borrower stops making payments on their loan, the lender is protected from any losses that may occur. MIP can be paid upfront or as part of the monthly mortgage payment and is typically a percentage of the loan amount. It is important to understand MIP when considering taking out a loan as it can have an impact on the overall cost of the loan. Knowing the details of MIP can help borrowers make more informed decisions about the type of loan they choose and the overall cost of their loan.

Advantages and Disadvantages of Mortgage Insurance Premium

Mortgage Insurance Premium (MIP) can be a helpful tool for those who are trying to buy a home, but there are both advantages and disadvantages to consider. The biggest advantage of MIP is that it is designed to reduce the amount of money you will need to put down when purchasing a home, meaning you can get into a home sooner than you would with a conventional loan. Additionally, it can provide the lender with additional security, meaning you may be able to get a lower interest rate or better terms on your loan. On the other hand, MIP can be expensive and typically requires you to pay an upfront premium, as well as ongoing premiums throughout the life of the loan. This can add up over time and make it more difficult to pay off your loan. Ultimately, it’s important to weigh the pros and cons of MIP before you decide if it’s the right choice for you.

How to Calculate Mortgage Insurance Premium

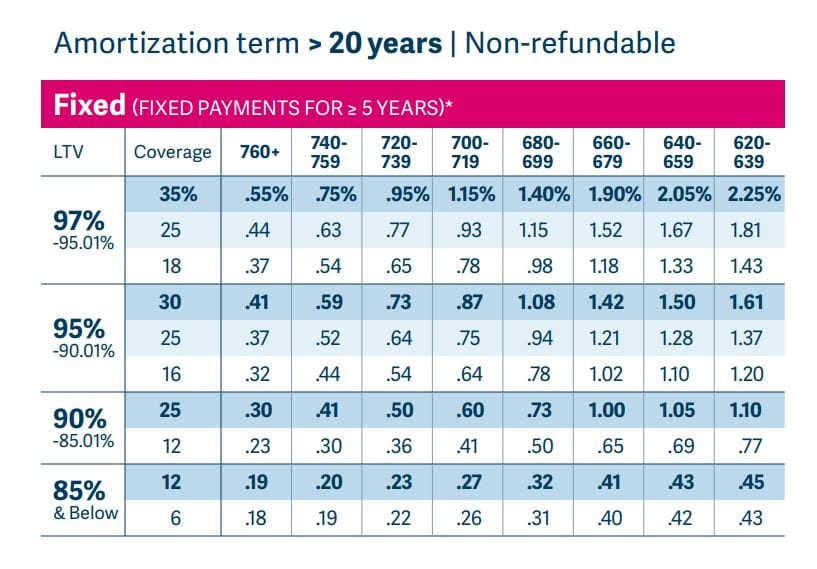

Calculating your mortgage insurance premium (MIP) can be a tricky process, but it doesn’t have to be! Knowing a few simple calculations and having a few helpful tips can make all the difference. To calculate your MIP, you’ll need to know the loan amount, the loan-to-value ratio and the term of the loan. Once you have those three, you can use the mortgage insurance premium calculator to get the exact amount of MIP for the loan. A few helpful tips to remember when calculating your MIP are to make sure you use the most up-to-date MIP rates and to double-check your calculations to make sure they are accurate. Taking the time to properly calculate your MIP can save you time and money in the long run, so don’t skimp on this important step!

Who Pays for Mortgage Insurance Premium?

Mortgage insurance premium (MIP) is an important part of the home buying process, but many people don’t know who pays for it. Generally, the borrower is responsible for paying the MIP, but there are exceptions. The amount of the MIP depends on the size of the down payment and the type of loan you choose. If you’re getting an FHA loan, you’ll be required to pay an upfront MIP and an annual MIP. If you’re getting a conventional loan, you may need to pay an upfront PMI premium, but you won’t be required to pay an annual PMI. If you’re getting a VA loan, you won’t have to pay any MIP. Knowing who pays for mortgage insurance premiums is important, so make sure you understand the loan you’re getting and the associated costs.

Is Mortgage Insurance Premium Tax Deductible?

Mortgage Insurance Premium (MIP) is an insurance policy that lenders require for borrowers who don’t have a large down payment or have bad credit. It’s a one-time fee that protects the lender if you can’t make your payments, and it’s usually a percentage of the loan amount. The big question is: is MIP tax deductible? The answer depends on the type of loan you have and when it was taken out. If you took out a loan before Dec. 31, 2017, the MIP may be deductible. If you took out a loan after Dec. 31, 2017, the MIP is not deductible. If you’re in the process of taking out a loan, make sure to check with your tax advisor to see if your MIP is tax deductible.