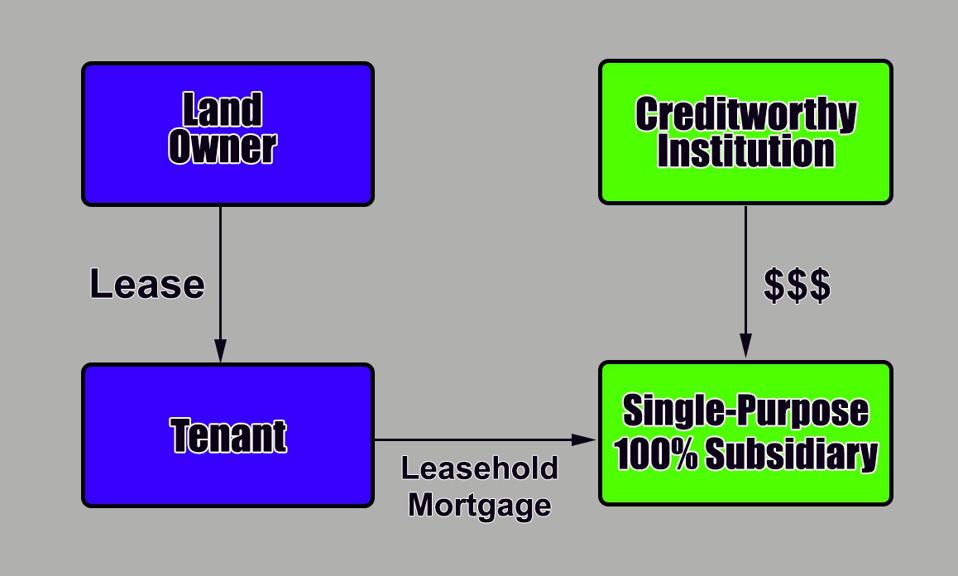

A leasehold mortgage is a powerful financial tool that can help landlords and tenants alike. It’s a way for landlords to remain in control of their property while also allowing tenants to access the funds they need for their own home. With a leasehold mortgage, tenants can purchase a property and make payments on it, even if the property is owned by someone else. This makes it a great option for landlords looking to increase their rental income without sacrificing ownership of their property. Learn more about leasehold mortgages and how they can benefit both landlords and tenants.

What Are the Benefits of a Leasehold Mortgage?

A leasehold mortgage can be a great way to get into homeownership if you’re on a budget. There are several benefits to taking out a leasehold mortgage, which include lower monthly payments, more flexible financing options, and the ability to build equity quickly. With a leasehold mortgage, you have the option to pay a smaller down payment, making it easier to afford the monthly payments. Additionally, you may be able to negotiate more flexible financing terms, such as a lower interest rate or longer repayment term. Finally, when you own the property, you can build equity quickly, which can increase your net worth and make it easier for you to take on other investments. All in all, a leasehold mortgage can be a great way to jumpstart your homeownership journey.

What Are the Risks of Taking Out a Leasehold Mortgage?

When you take out a leasehold mortgage, you are taking on a significant amount of risk. With a leasehold mortgage, you are essentially taking out a loan that is backed by the land you’re leasing, rather than the property itself. This means that if the land is not paid off, or if it is foreclosed upon, you can lose the property and whatever money you invested in it. Additionally, because a leasehold mortgage is secured by the land, you may have to pay higher interest rates than a traditional mortgage. Lastly, since the land is not owned outright, there is a chance that the land you’re leasing could be sold to someone else, leaving you without a place to live or conduct business. For all these reasons, it’s important to weigh the risks carefully before taking out a leasehold mortgage.

What Are the Different Types of Leasehold Mortgages?

Leasehold mortgages come in a variety of shapes and sizes, so it’s important to know the different types of leasehold mortgages available to you. The most common type of leasehold mortgage is the traditional mortgage, which is taken out for a fixed period of time and repaid with monthly payments. A second type of leasehold mortgage is the adjustable rate mortgage, which allows you to adjust the interest rate and repayment terms to fit your budget. Finally, there is the interest-only leasehold mortgage, which allows you to make interest payments only, with no principal payments. Each of these leaseshold mortgages has its own advantages and disadvantages, so it is important to consider all of your options before making a final decision.

How to Qualify for a Leasehold Mortgage?

If you’re looking to purchase a leasehold property, you may be wondering if you qualify for a leasehold mortgage. Qualifying for a leasehold mortgage is similar to qualifying for any other type of mortgage, but there are some key differences to keep in mind. To qualify for a leasehold mortgage, you’ll need to have a good credit score, a reliable source of income, and a down payment of at least 20%. You’ll also need to provide information about your lease, such as the length of the lease, any restrictions or fees, and the current market value of the property. Lastly, you’ll need to show that you can afford the mortgage payments, which may be higher than a traditional mortgage due to the shorter lease term. Taking all of these factors into consideration, you can determine if you qualify for a leasehold mortgage and begin the process of purchasing your dream home.

How to Compare Different Leasehold Mortgage Options?

Comparing different leasehold mortgage options can be a daunting task. With so many different options available, it’s important to carefully weigh the pros and cons of each one to ensure you make the best decision for your financial future. When looking at leasehold mortgage options, it’s important to consider things like interest rates, repayment terms, and any other fees associated with the loan. Additionally, it’s important to compare the different lenders available and to make sure the lender you choose is reputable and trustworthy. Doing your due diligence will help you make the best decision possible when it comes to a leasehold mortgage.