Discover the intricacies of mortgage insurance as we dive into an enlightening exploration of its pros and cons. Whether you’re a first-time homebuyer or a seasoned property investor, understanding the ins and outs of this financial safety net is crucial to your long-term success. Unravel the benefits and drawbacks of this essential home-ownership tool, as we provide you with an unbiased and comprehensive analysis that will empower you to make well-informed decisions for your financial future. Get ready to unlock the secrets of mortgage insurance and set yourself on the path to a secure and prosperous home-ownership journey.

Enables homebuyers with lower down payments: Mortgage insurance allows prospective homeowners to purchase a house with a smaller down payment, as low as 3-5% of the home’s value

Mortgage insurance plays a crucial role in empowering aspiring homeowners by enabling them to buy a home with lower down payments. Typically, lenders require a 20% down payment; however, mortgage insurance reduces this threshold to as low as 3-5% of the property’s value. This benefit opens doors to homeownership for a broader range of individuals, including first-time buyers and those with limited savings. Consequently, this increased accessibility to the housing market fosters economic growth and helps families achieve their dream of owning a home. Overall, mortgage insurance acts as a catalyst for financial stability and social mobility, contributing to a thriving real estate market.

This makes homeownership more accessible for those who might not have the necessary savings for a larger upfront payment.

Mortgage insurance offers a valuable opportunity for aspiring homeowners who may struggle to save for a substantial down payment. By providing access to low-down-payment mortgages, this insurance enables individuals to achieve the dream of homeownership sooner than they might have thought possible. In turn, this helps to promote financial stability and long-term wealth-building, as homeowners can start building equity in their property earlier. Furthermore, mortgage insurance can also benefit the housing market overall, as it allows more people to enter the market and encourages growth. However, borrowers should carefully weigh the costs and benefits of mortgage insurance to determine if it is the right choice for their financial situation.

Protects the lender: Mortgage insurance provides a level of protection for the lender, as it covers a portion of the loan in case of default

A significant advantage of mortgage insurance is the protection it offers to lenders by minimizing their financial risks. In the unfortunate event of a borrower defaulting on their loan, mortgage insurance covers a portion of the outstanding balance, safeguarding the lender’s investment. This added security encourages lenders to approve mortgage applications from borrowers with lower down payments or credit scores, ultimately expanding homeownership opportunities for many individuals. By assuring lenders of a safety net, mortgage insurance plays a crucial role in maintaining a stable housing market, fostering economic growth, and promoting financial inclusion.

This security encourages lenders to offer loans to a wider range of borrowers, including those with lower credit scores or higher debt-to-income ratios.

Mortgage insurance undoubtedly expands opportunities for potential homebuyers by providing a safety net for lenders. This financial security allows lenders to confidently offer mortgage loans to a diverse pool of borrowers with varying financial backgrounds, including those with lower credit scores or higher debt-to-income ratios. Consequently, this increases the overall accessibility of homeownership, as individuals who may not have qualified for a loan under traditional circumstances now have the chance to secure a mortgage. Additionally, the increased competition among borrowers encourages mortgage lenders to offer more favorable loan terms and interest rates, contributing to the growth and stability of the housing market.

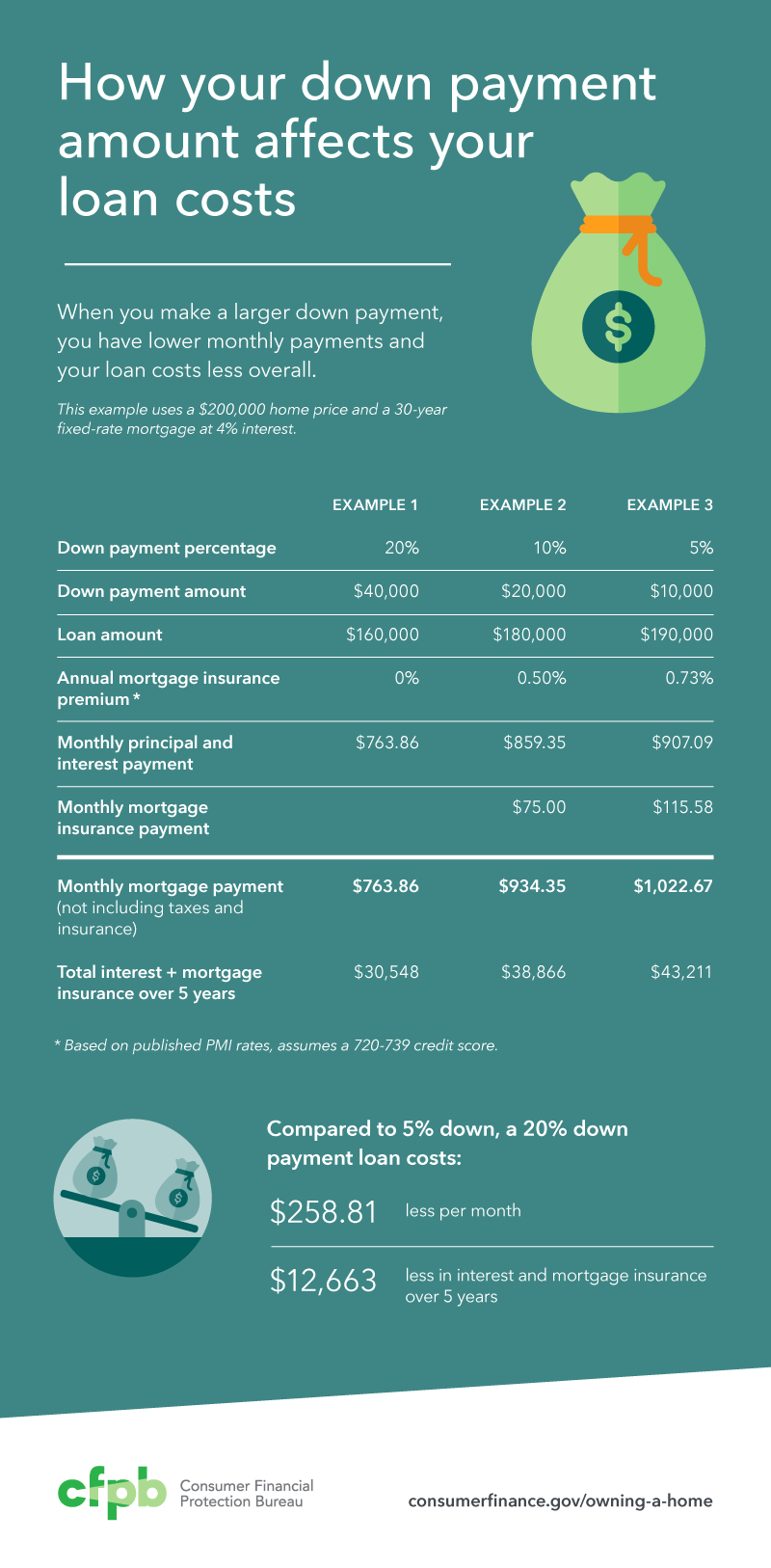

Potential for lower monthly payments: For some borrowers, the cost of mortgage insurance might be lower than the additional interest they would

![]()

One of the key advantages of mortgage insurance is the potential for lower monthly payments. In certain cases, homebuyers may find that the cost of mortgage insurance is less than the extra interest they would incur without it. This is particularly true for those with a smaller down payment or a less-than-stellar credit history, as they often face higher interest rates on their mortgage loans. By opting for mortgage insurance, these borrowers can effectively lower their overall monthly expenses, making homeownership more affordable and accessible. Therefore, it is crucial for potential buyers to carefully weigh the costs and benefits of mortgage insurance when deciding on their mortgage financing options.