A mortgage is one of the most important financial decisions you will ever make. It can be a daunting process, but understanding how mortgages work and the steps involved can help make the process easier. In this article, we will explore what a mortgage is, the different types available, and the steps involved in securing one. We’ll also discuss the importance of seeking professional advice and the role of credit scores and down payments. With this knowledge, you’ll be in a better position to make an informed decision when it comes to choosing the right mortgage for you.

What is a Mortgage and What Does it Involve?

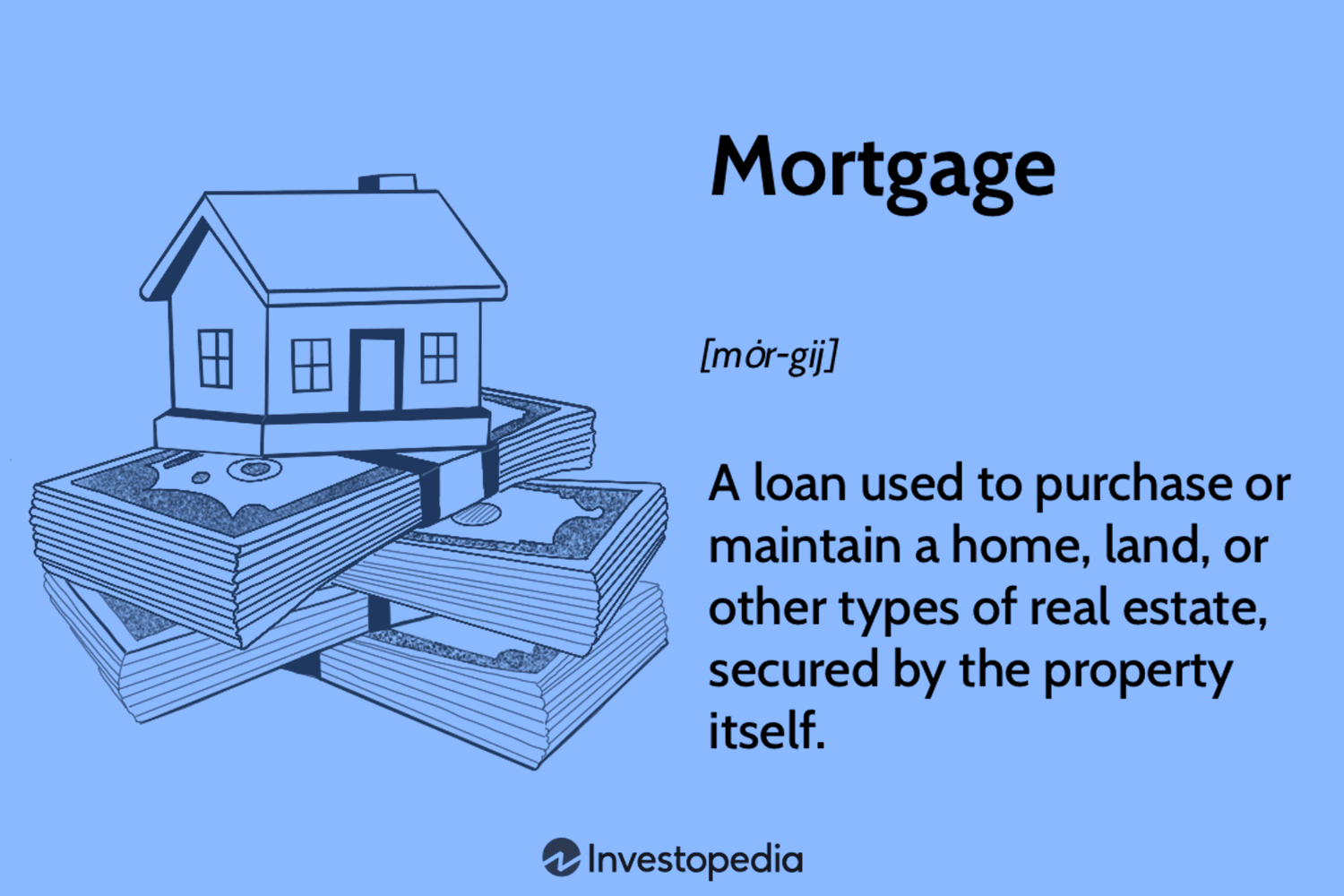

A mortgage is a loan used to purchase a home. It is a legal agreement that allows a borrower to borrow money from a lender in exchange for a lien on the property. The borrower is then responsible for repaying the loan, usually over an extended period of time, usually 15 to 30 years. The lender will typically require a down payment, typically 10-20% of the total loan amount. The borrower must also pay closing costs, which may include points (a fee charged for the loan) and origination fees (a fee charged for processing the loan). The borrower will also be required to pay interest on the loan each month. The interest rate on the mortgage is determined by the lender and can vary from lender to lender, depending on the borrower’s credit score, loan amount, and other factors. The borrower will also be required to pay taxes, insurance, and other costs associated with the loan. Once the loan is paid off, the borrower will no longer owe the lender money and will have complete ownership of the property.

Different Types of Mortgages and Their Benefits

Different types of mortgages offer a variety of benefits to borrowers depending on their individual financial goals and needs. Fixed-rate mortgages offer the stability of a set interest rate over the life of the loan and are the most popular type of mortgage. They are ideal for borrowers who plan to stay in their home for a long period of time and want to know their payment amount will remain the same. Adjustable-rate mortgages, or ARMs, offer borrowers a lower initial interest rate with the chance for rate adjustments over the life of the loan. ARMs are ideal for borrowers who plan on staying in their home for a short period of time and are comfortable with the risk of fluctuating payments. Other types of mortgages include government-insured mortgages, like Federal Housing Administration (FHA) loans and Veterans Affairs (VA) loans, which offer borrowers the ability to purchase a home with a lower down payment and more lenient credit requirements. Jumbo loans are available for higher-priced homes and require a higher down payment than conventional loans. FHA 203k loans are specialized home improvement loans that allow borrowers to finance repairs and improvements into the loan amount. Each type of mortgage has its own set of benefits and drawbacks, so it’s important for borrowers to research

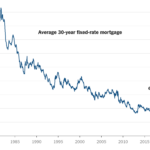

Understanding Mortgage Rates and Interest

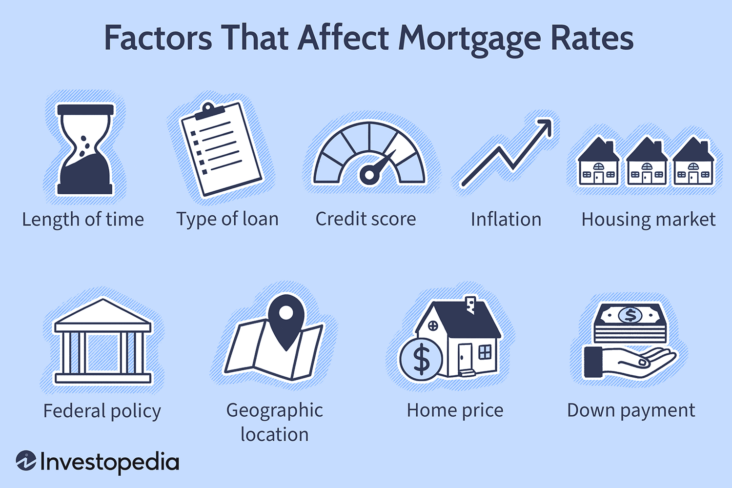

Understanding mortgage rates and interest is an essential part of the home buying process. Mortgage rates and interest can vary greatly depending on a variety of factors, such as the current market conditions, the type of loan you are getting, the terms of the loan, and your credit score. Mortgage rates are determined by a variety of economic indicators, including inflation rates, employment figures, economic growth, and other market forces. The Federal Reserve can also play a role in mortgage rates and interest by changing the federal funds rate. Generally, when the federal funds rate increases, so do mortgage rates. The type of loan you choose also affects the mortgage rate and interest. For example, adjustable-rate mortgages typically have lower initial interest rates, but the rate and payments can change over time. Fixed-rate mortgages, on the other hand, have a fixed interest rate for the life of the loan, meaning your rate and payments will never change. Your credit score also affects the mortgage rate and interest you receive. Generally, the higher your credit score, the lower the interest rate you will receive. Your credit score is determined by a number of factors, including your payment history, credit utilization rate, age of credit, and more.

The Mortgage Application Process

The mortgage application process is an important step in the home buying journey. It involves gathering your financial documents, such as proof of income, tax returns, bank statements, credit reports, and more. You will then submit a detailed loan application to a lender of your choice. The lender will review your documents and assess your creditworthiness. If you are approved, the lender will create a loan contract and provide you with an estimate of the closing costs. Once you are ready to close on your mortgage, the lender will facilitate the process of transferring the title and funds.When applying for a mortgage, it’s important to shop around and compare rates and terms before committing to a lender. Different lenders have different requirements and can offer different products. It’s important to ask questions and get clarity on the loan process, such as what type of loan you’re applying for, the payment terms, and any additional fees or closing costs. Doing your research and being knowledgeable about the process can help you find the best loan for your needs.

How to Save Money on Your Mortgage

Saving money on your mortgage can be a great way to reduce your monthly payments, free up some cash for other expenses, or just to leave more money in your pocket. One of the best ways to save money on your mortgage is to shop around for the best interest rate. Different lenders may offer different interest rates on the same loan, so it pays to shop around. Additionally, you may be able to take advantage of discounts or other incentives offered by certain lenders. If you have an existing loan, you may be able to refinance to a lower rate. Another way to save money on your mortgage is to make additional payments or to make payments more frequently. Making a payment twice a month instead of once can help you pay down the loan more quickly, and you can save a significant amount of interest. Making extra payments on the principal will also reduce your loan balance and the amount of interest you pay over time. Lastly, you should consider the type of mortgage you have. Adjustable-rate mortgages can be attractive in the short term, but they can also increase your payments over time. Choosing a fixed-rate mortgage may be a better choice in the long run, as your payments will remain the same for the life of the