If you’re in the market for a home, chances are you’ve been trying to figure out how to calculate mortgage payments. It can be a daunting task, but with the right information and guidance, you can easily figure out the monthly payments you’ll need to make. In this article, we’ll show you how to calculate mortgage payments and provide useful tips for understanding the process. Read on to learn more about how to effectively calculate mortgage payments and make the most of your homebuying experience.

Understanding the Basics of Mortgage Calculations

Understanding the basics of mortgage calculations can help borrowers make informed decisions when shopping for the right mortgage. It’s important to understand the different factors that affect mortgage payments, such as the loan amount, interest rate, and loan term. Additionally, potential borrowers should be aware of the fees associated with a mortgage, such as closing costs, origination fees, and private mortgage insurance. Knowing the basics of how mortgages are calculated can also help borrowers make sound decisions about how much of a mortgage they can afford. Calculating the total cost of a mortgage can help borrowers understand the true cost of a loan, and make sure they are not overpaying for their mortgage. With the knowledge of how mortgage payments are calculated, borrowers can choose the best loan for their needs and budget.

Breaking Down the Mortgage Payment Formula

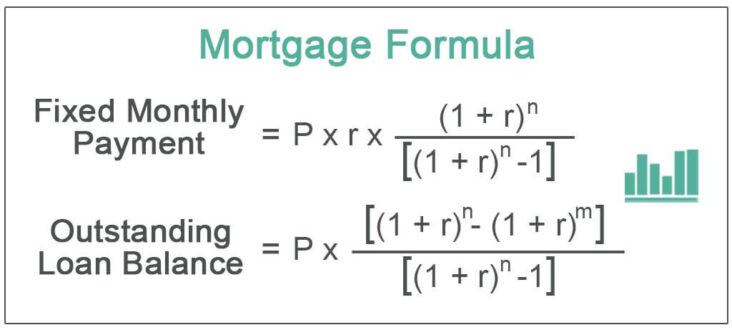

Mortgage payments can be a daunting concept, especially when it comes to understanding the formula and calculating the amount of the payments. Breaking down the mortgage payment formula can be a useful tool to help understand how the payments are calculated. The formula is composed of four main components: principal, interest rate, term, and payment. The principal is the amount of the loan that is unpaid. This is the amount that is borrowed, and the amount that will be paid back over the course of the loan. The interest rate is the percentage of the principal that will be paid in interest over the life of the loan. The term is the length of time that the loan will last. The payment is the amount that will be paid on a regular basis to pay back the loan. The formula for calculating a mortgage payment is: Payment = Principal x (Interest Rate / 12) / (1 – (1 / (1 + Interest Rate / 12) ^ (Term * 12)). This formula allows for the principal, interest rate, term, and payment to be put into the equation to calculate the monthly mortgage payment. Taking the time to understand this formula and breaking it down into its components can be a helpful tool in understanding how mortgage payments are calculated.

Examining Additional Factors that Impact Mortgage Payments

When calculating mortgage payments, there are several additional factors that could influence the amount due each month. Homeowners need to consider the cost of taxes and insurance, which can significantly affect the total amount due. Additionally, they should review their local state and federal laws to ensure that they are in compliance with any applicable regulations. It is also important to factor in the interest rate, which can vary depending on the type of loan and the lender. Other factors such as the loan term, down payment, and points should be taken into account as well. Understanding all of these factors can help homeowners get the most out of their mortgage and ensure that they can make their payments on time.

Using Online Mortgage Calculators as a Tool

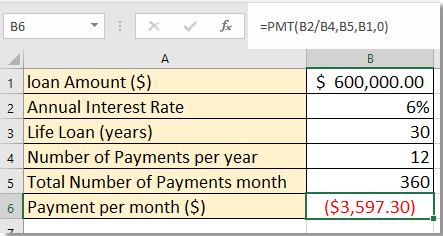

Using online mortgage calculators can be a great tool for quickly and easily finding out how much your mortgage payments could be. Most online mortgage calculators will ask for basic information such as the loan amount, interest rate, and loan term. With this information, the calculator will then calculate your estimated monthly mortgage payments. The calculator will also provide you with information regarding your total interest payments, total home payments, and the total amount of money you will pay over the life of the loan. Knowing this information can help you plan your financial future, as it will give you an idea of how much you will need to save up for a down payment. Additionally, it can help you budget your monthly payments so that you can make sure you are able to make them on time. By taking the time to use a mortgage calculator, you can ensure that you are getting the most out of your loan and that you are making a responsible decision when it comes to your finances.

Tips for Reducing Mortgage Payments and Saving Money

Saving money and reducing mortgage payments is a priority for many homeowners. Fortunately, there are several ways to reduce the amount you owe on your mortgage without refinancing. Here are some tips to help you save money on your mortgage payments:1. Make extra payments: Making extra payments can reduce your loan balance quickly and save you interest over the life of the loan. Be sure to make sure your payments are applied toward the principal, not the interest. 2. Increase your monthly payments: Making larger payments each month can also save you money. By paying a little extra each month, you can reduce the amount of interest you owe and pay off your mortgage faster.3. Refinance: Refinancing your mortgage can potentially lower your payment and save you money. It is important to consider the costs associated with refinancing, such as closing costs and other fees.4. Get a lower interest rate: You can shop around for a lower interest rate that can reduce your payments and save you money over the life of the loan. Keep in mind that if you have a fixed-rate mortgage, you may have to pay a penalty for refinancing.By following these tips, you can reduce mortgage payments and save money.