Are you in the market for a mortgage? Do you want to make sure you don’t make any costly mistakes that could lead to financial problems down the road? In this article, we will discuss the most common mortgage mistakes and how to avoid them. We will look at everything from choosing the wrong loan type to failing to read the fine print. With this information and tips, you can make sure you get the best mortgage for you and your family and avoid common pitfalls.

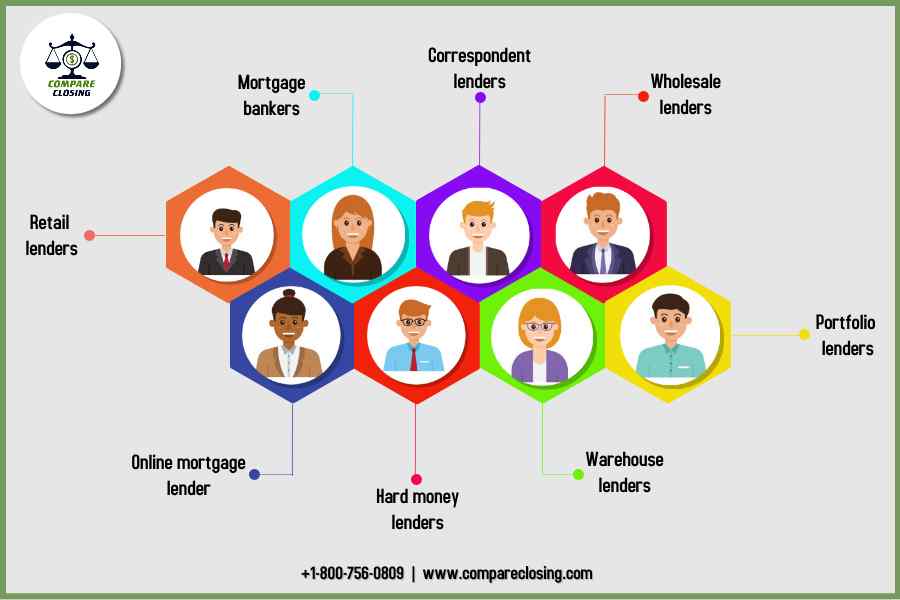

Not Shopping Around for the Best Rates: Shopping around for the best rates can save you thousands of dollars over the life of your loan

When it comes to shopping around for the best rates, it’s important to take the time to do some research. Start by looking at the rates offered by different lenders, and make sure to compare their fees and other costs associated with the loan. It’s also a good idea to check out online lenders, as they often offer more competitive rates than more traditional lenders. Additionally, you can look for special offers such as cash-back rewards or lower closing costs. Once you’ve identified the best rate and terms for your loan, make sure to read the fine print to make sure you understand all the details before signing anything. Taking the time to shop around for the best rates can save you thousands of dollars over the life of your loan, so it’s well worth the effort.

Be sure to compare different lenders to get the best deal.

When shopping for a mortgage, it’s important to compare different lenders to get the best deal. Working with a trusted, knowledgeable lender is the best way to ensure you get the best rate and terms. Researching a few lenders and comparing their rates, fees, and loan products can save you thousands in the long run. It’s important to keep in mind that the lowest rate isn’t always the best deal. Consider the fees, loan term, and repayment options before making a decision. A reputable lender will be happy to answer your questions and provide you with helpful information. By doing your due diligence and comparing lenders, you can make an educated decision on which mortgage is right for you.

Not Exploring All Financing Options: There are many different types of mortgages available, from fixed-rate to adjustable-rate, and from government-backed loans to conventional loans

When it comes to mortgages, there is no one-size-fits-all solution. That’s why it’s important to explore all financing options before making a decision. There are a variety of mortgages available, such as fixed-rate, adjustable-rate, government-backed, and conventional loans. Each of these mortgages offer different advantages and disadvantages, and it is important to know what type of loan best suits your needs. Fixed-rate mortgages provide stability, as the interest rate stays the same for the entire life of the loan. Adjustable-rate mortgages can be more beneficial for those who are expecting an increase in their income over time, as the interest rate adjusts to the current market rate. Government-backed loans, such as FHA and VA loans, offer more lenient requirements for borrowers with lower incomes or credit scores. Finally, conventional loans are more suited for those who have higher incomes and good credit scores. It is important to do your research and explore all financing options before making a decision. By understanding the different types of mortgages available, you can make an informed decision that best suits your financial needs.

Be sure to explore all of your options to find the best fit for your financial situation.

When it comes to making a mortgage decision, it is important to take the time to explore all of your options to find the best fit for your financial situation. Don’t just settle for the first loan you find. By researching different types of loans, interest rates, and repayment terms, you can find the loan that works best for your budget and long-term goals. When you are shopping for a loan, be sure to compare rates, terms, and fees to make sure you are getting the best deal. Additionally, be sure to ask questions to make sure you understand the loan and don’t forget to factor in all the costs associated with the loan, such as closing costs and other fees. Taking the time to find the right loan can help you save money and avoid costly mistakes.

Not Understanding Mortgage Terms: Make sure you understand the terms of your mortgage before you sign anything

Not understanding the mortgage terms can be one of the most costly mistakes that borrowers make when applying for a mortgage. To avoid this mistake, it is important to do your research and really understand the terms before signing anything. Make sure you understand the interest rate, the terms of the loan, and the fees associated with the loan. It is also important to understand any prepayment penalties, the repayment schedule, and other details. Taking the time to understand all of these factors can help you make sure that you are getting the best deal for your mortgage. Speak to a mortgage broker or an experienced financial advisor if you have any questions about the terms of your loan. Taking the time to understand the terms of your mortgage will help you save money in the long run and ensure that you are getting the best deal for your mortgage.

Ask your lender for clarification if you don’t understand something and never sign a document without reading it.

When it comes to mortgage mistakes, one of the most important things to do is to make sure you understand everything your lender is telling you. If something is unclear, don’t be afraid to ask for more information. Your lender should be willing to answer any questions you have and explain in detail any part of the mortgage process you don’t understand. It is also important to never sign a document without reading it thoroughly. Make sure you understand the terms and conditions of the mortgage and ask questions if anything is unclear. Doing your due diligence before signing any documents can help you avoid costly mistakes and make sure you get the best possible mortgage deal. By taking the time to ask questions and make sure you understand your lender’s terms and conditions, you can ensure you make the right decision when it comes to your mortgage.

Not Reviewing Your Credit Report: Before applying for a mortgage, make sure you review your credit report and fix any mistakes

It is essential to review your credit report before applying for a mortgage. This document contains information about your financial history, such as payment history, debt, and other financial activities. You should look for any mistakes that may hurt your credit score, as your credit score is one of the most important factors when lenders consider approving you for a mortgage. To check your credit report, you can contact the three major credit bureaus, Experian, Equifax, and TransUnion, which are required by law to provide you with a free credit report once a year. If you find any errors, you can dispute them with the credit bureaus and have them corrected. This will help you improve your credit score and increase your chances of getting approved for a mortgage. Taking the time to review your credit report and fix any mistakes can save you time and money in the long run.

A low credit score can result in a higher interest rate or even a denial of your loan.

A low credit score can have a major impact on your ability to secure a mortgage loan. If you have a low credit score, it may be difficult to obtain a loan at all, or you may only be able to qualify for a loan with a much higher interest rate. Before applying for a mortgage, it is important to ensure that your credit score is as high as possible. This can be done by paying your bills on time, reducing your debt-to-income ratio, and avoiding taking on too much debt. Additionally, it is important to review your credit report for any errors or incorrect information that may be negatively affecting your score. Taking these steps can help you to avoid being denied a loan due to a low credit score, and help you to obtain the best interest rate possible.

Not Setting a Realistic Budget: Be sure to create a realistic budget and stick to it

Setting a realistic budget is an essential part of the mortgage process. Before you begin the house-hunting process, it’s important to determine what you can afford. Start by looking at your budget and calculating your income, expenses, and debt. Consider all of your financial commitments and make sure you can comfortably afford a mortgage. Once you have a realistic budget, stick to it and don’t get tempted to spend beyond your means. If you’re ever unsure about whether a house is within your budget, it’s best to err on the side of caution and wait until you have more financial freedom. A mortgage is a long-term commitment, so it’s important to make sure you can comfortably afford it before you sign on the dotted line.

This will help you determine how much house you can afford and will prevent you from taking on more debt than you can handle.

When it comes to mortgages, it’s important to know how much house you can afford. Overspending on a mortgage can lead to a financial burden that can be difficult to manage. Before taking on a mortgage, it’s important to consider your current financial situation and determine how much you’re able to commit to a monthly mortgage payment. Additionally, it’s important to factor in other expenses such as taxes, insurance, and utilities to ensure you’re comfortable with the amount of debt you’re taking on. Taking the time to calculate the total cost of a mortgage will help ensure you don’t end up in a situation where you’re unable to make payments. Additionally, budgeting for unexpected costs is a good way to make sure you’re prepared for any additional fees that may come up during the loan process. By taking the time to review your finances and plan accordingly, you’ll be able to avoid taking on more debt than you can handle.