Are you tired of shelling out hundreds of dollars each month for Private Mortgage Insurance (PMI)? You’re not alone! Many savvy homebuyers are looking for ways to dodge this pesky expense, and we’re here to help. In this comprehensive guide, we’ll reveal the top strategies for avoiding PMI, so you can keep more money in your pocket while still achieving your dream of homeownership. From exploring various loan options to leveraging creative financing methods, these expert tips will pave the way for a PMI-free future. Read on to discover the insider secrets to bypassing PMI and start saving big on your mortgage today!

Save for a larger down payment: The simplest way to avoid PMI is by putting down at least 20% of the home’s purchase price as a down payment

One of the most effective strategies to bypass private mortgage insurance (PMI) is to save diligently for a more substantial down payment. By accumulating a minimum of 20% of the property’s purchase price, you can significantly reduce your mortgage-related expenses and demonstrate your financial stability to lenders. This not only eliminates the need for PMI but also lowers your monthly mortgage payments and improves your chances of securing favorable loan terms. To achieve this goal, consider creating a disciplined savings plan, exploring various investment opportunities, and cutting back on unnecessary expenses, all while keeping your focus on the long-term benefits of homeownership without the burden of PMI.

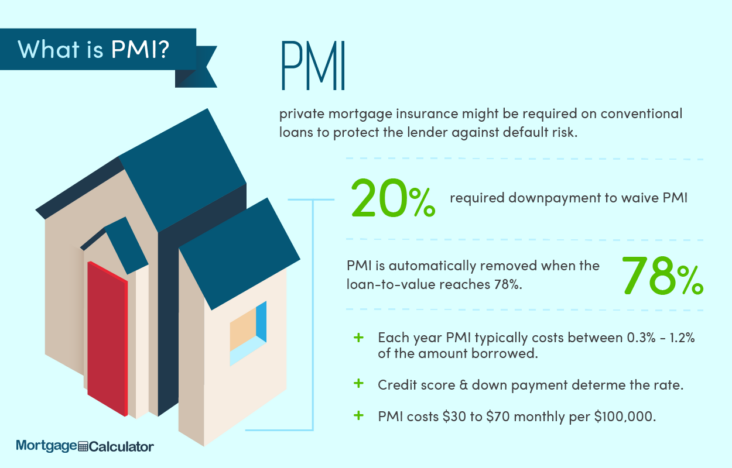

This will automatically eliminate the need for PMI, as lenders typically only require it for loans with a loan-to-value (LTV) ratio of 80% or higher.

One of the most effective strategies to bypass Private Mortgage Insurance (PMI) is to maintain a lower loan-to-value (LTV) ratio, ideally below 80%. Lenders typically mandate PMI for loans with an LTV ratio of 80% or more, as it safeguards them against potential borrower defaults. To accomplish this, homebuyers should aim to make a larger down payment, which not only reduces the need for PMI but also results in lower monthly mortgage payments. By diligently saving and budgeting for a more substantial down payment, homebuyers can successfully avoid PMI, ultimately saving thousands of dollars during the lifetime of their mortgage.

Opt for a piggyback loan: A piggyback loan, also known as an 80-10-10 loan, involves taking out two separate loans for your home purchase – one for 80% of the home’s value and another for 10% of the value

Opt for a piggyback loan to bypass PMI and save on your mortgage expenses. A piggyback loan, or an 80-10-10 loan, is a strategic method where you take out two distinct loans for your home purchase – one loan covering 80% of the property’s value and another for 10% of the value. By doing this, you can avoid PMI since your primary mortgage will be below the 80% loan-to-value threshold. Furthermore, piggyback loans offer flexibility, allowing you to choose between a fixed or adjustable interest rate for the second loan. Explore this alternative financing option and keep your mortgage costs down while sidestepping PMI.

The remaining 10% will be covered by your down payment

In order to successfully avoid PMI (Private Mortgage Insurance), it is essential to make a strategic down payment. Typically, lenders require a down payment of 20% for a conventional mortgage to waive PMI. However, a popular strategy is to opt for an 80-10-10 loan, where 80% of the home’s value is covered by the first mortgage, 10% is covered by a second loan, and the remaining 10% is covered by your down payment. This approach not only helps you bypass the need for PMI, but also enables you to secure favorable mortgage terms, ultimately reducing your overall home financing costs and providing a solid foundation for homeownership.

Since the primary loan is for

One of the most effective strategies to avoid paying Private Mortgage Insurance (PMI) is by keeping your primary loan amount below 80% of your home’s value. This can be achieved by making a larger down payment or exploring alternative loan options that cater to your financial needs. By doing so, you not only save on the costs associated with PMI, but you may also qualify for better interest rates, reducing your overall mortgage expenses. In addition, maintaining a strong credit score and shopping around for the best mortgage deals can significantly increase your chances of securing a loan without the burden of PMI.