Reverse mortgages can be a great way to help seniors secure their financial independence during retirement. But how exactly do they work? In this article, we will explore the basics of reverse mortgages, from how to qualify to the different types of loans available and their potential benefits and drawbacks. With a better understanding of how reverse mortgages work, you can make an informed decision about whether this type of loan is right for you.

What is a Reverse Mortgage?

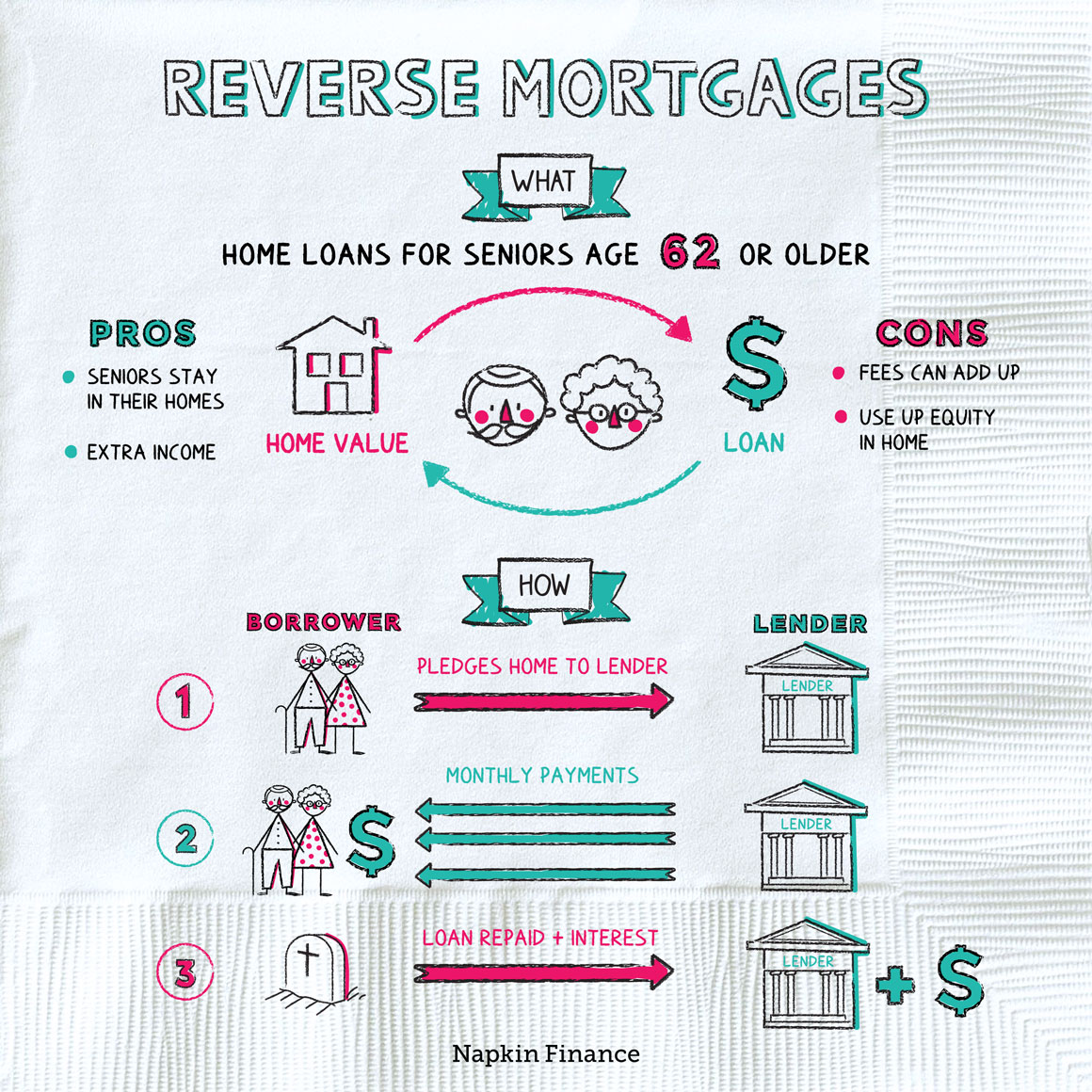

.What is a Reverse Mortgage? A reverse mortgage is a loan that allows homeowners over the age of 62 to access their home equity without having to make any monthly mortgage payments. This loan is secured by your home and allows you to borrow against its value without selling it or taking on new debt. With a reverse mortgage, you can receive monthly payments, a lump sum, or a line of credit to use as you need. The amount you can borrow is based on your age, the value of your home, and current interest rates, and you are not required to pay it back until you leave the home. Reverse mortgages are a great way to access money to pay for medical bills, home improvements, or other expenses in retirement.

Benefits of a Reverse Mortgage

Reverse mortgages can be a great option for retirees who are looking to supplement their income and want to stay in their homes. With a reverse mortgage, you can access the equity in your home without having to make regular payments. This can be a great way to get access to cash without having to worry about making a traditional mortgage payment. Additionally, reverse mortgages are also known for their tax benefits. With a reverse mortgage, you don’t have to pay taxes on the money you receive, so you can use it to pay off debts or improve your home without worrying about extra taxes. Finally, reverse mortgages also offer increased financial security, as they can provide you with an extra source of income to help you stay in your home and enjoy the life you want.

Qualifying for a Reverse Mortgage

Qualifying for a reverse mortgage is a great way to unlock the equity you have in your home. To qualify for a reverse mortgage, you must be at least 62 years old, own your home outright or have a low loan balance, and be able to show that you can make payments on any existing mortgage or property taxes. Additionally, you need to be able to show that you can afford to maintain the home and keep up with its taxes and insurance payments. To make sure you are able to meet these qualifications, you may need to get a financial assessment from a reverse mortgage lender. This assessment looks at your income, credit history, and other factors to make sure you are able to make the payments on a reverse mortgage. Once you have been approved, you can start enjoying the benefits of a reverse mortgage, such as a steady stream of income and the ability to stay in your home.

Disadvantages of a Reverse Mortgage

Reverse mortgages are a great way to access the equity in your home without having to make regular payments, but they definitely aren’t without their drawbacks. One of the biggest disadvantages of a reverse mortgage is the high fees associated with them. Origination fees, closing costs, servicing fees, and mortgage insurance premiums can add up quickly, making it a costly loan to get into. On top of that, the amount of money you can borrow is usually much lower than a traditional loan. Another thing to consider is that the loan must be paid back eventually. If the borrower passes away or the home is sold, the loan must be paid off with the proceeds from the sale. Finally, the interest rate on a reverse mortgage is typically higher than a traditional loan. All of these factors should be carefully weighed before taking out a reverse mortgage.

Repaying a Reverse Mortgage

Repaying a reverse mortgage is a simple process that can be done in a variety of ways. For starters, you can choose to pay the loan off in full when it is due, either through your own funds or those of an estate. This is a great option if you have built up enough equity in your home to cover the loan amount. You can also establish a repayment plan with the lender, where you pay back the loan in regular installments. This is a great option if you have a steady income and want to keep your home for a longer period of time. It is also important to note that you do not have to make monthly payments on a reverse mortgage. Instead, you are only responsible for paying back the loan when it is due, either in full or in part. This means you can remain living in your home until it is paid off.